Aluminium 2018, a Window On the World of Aluminium

A positive outlook for the future of aluminium, even though the tariff and sanctions war acts as a fetter. A conversation with All.co and HTA’s Managing Director, Simonetta Vecoli, on the future of the industry following Aluminium 2018 in Düsseldorf

by Mario Conserva

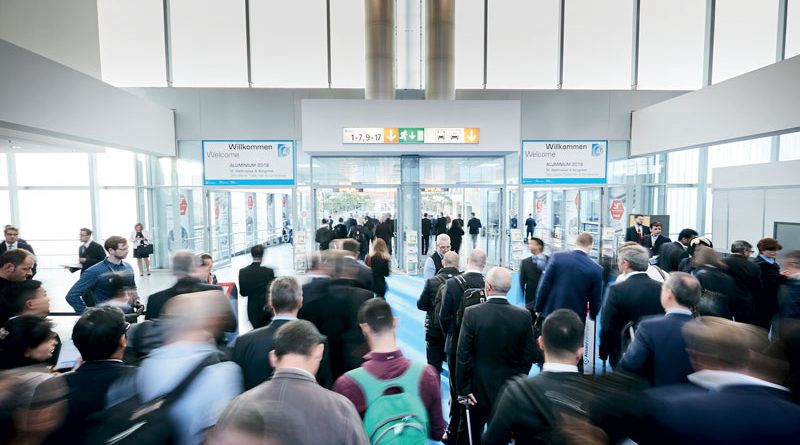

The twelfth edition of the Aluminium Trade Fair came to an end in Düsseldorf with a successful outcome in terms of visitor turnover and with 971 exhibitors: first of all from Germany (307 companies) followed by Italy (118) and China (103), Turkey (64), Austria and Spain (32), the United States (29), Holland (25), France and the United Kingdom (23) and Canada (19). Over 24,000 visitors were recorded, practically confirming the 2016 datum. The positive trend of this event reflects positive expectations regarding aluminium, a material which seems to be destined to further progress worldwide, with very high forecast growth rates in the areas currently characterized by modest per capita metal consumption, such as, many parts of Asia and the African continent. On the other hand, even for a mature market such as old Europe, a considerable increase is envisaged in the demand of primary metal in the next few years, as confirmed by the study carried out by Rome’s LUISS university dedicated to the light metal’s industrial system and particularly to the EU downstream industries of processors and end users, which represents around 90% of the entire aluminium industrial system. We interviewed many of the Italian and foreign exhibitors and guests at Aluminium, with the main purpose of verifying the degree of trust in the industry in a moment of strong international tensions for the light metal system, ranging from the tariff war to sanctions on Russian metal. We shall report the exchange of ideas which we had with Simonetta Vecoli, managing director of All.co and of HTA, the group’s company based in Pontedera (near Pisa) dedicated to extrusions for industrial purposes.

What are your impressions regarding this edition of Aluminium?

An excellent show, which summons important segments of the aluminium industry, referring particularly to the upstream productions, extrusion and rolling; the event is well-organized as usual and capable of attracting many visitors. It is clear that the strength of the German market is in itself a very important element, suffice it to think about the extrusion figures. About ten years ago internal consumption of aluminium profiles were not very different in Italy and Germany, now the ratio is almost of 1 to 3, and this is why European and extra-European transformers study the German market. The same applies to all other industrial sectors of the light metal, even though here in Düsseldorf the foundry world was not as present, compared, for instance, to what can be seen in Italy at Metef. At any rate, although we are talking about a successful show, this edition did not resonate with the same positive atmosphere as in other editions, there might be some fatigue, international issues or perhaps uncertainties referred to the trade of the metal, from tariffs to sanctions, might have dampened enthusiasm to some extent.

What type of outlook for aluminium emerges especially from the meetings, congresses, different more or less official standpoints of the market’s main players present in Düsseldorf?

There is nothing new under the sun, the usual confirmation of an aluminium market which is globally growing, the prospect of coming close to 110 million tons of primary metal produced in the world within thirty years, compared to the 2017 datum which is only slightly above 63 million tons, the strong development of consumption in such classic segments as transportation, construction and packaging, the great attention paid to recycling within the framework of an increasingly circular economy, the continuous and constant rise of the stakes especially for the European market, in terms of overall expected quality of the materials produced and services offered to clients.

Regarding the extrusion market, are there any particular issues worth highlighting?

In general we can say that, following a good 2017, the current year has been positive for the first three quarters, then things suddenly stopped; it is evident that the tariff war started off by the US administration, followed by chaos on the market created by sanctions against Rusal, were triggering factors for a state of anxiety which deeply influenced the demand and supply of raw material and semis. We should not forget that the European Union lacks enormous amounts of primary metal and that Rusal’s metal has traditionally been an essential source, fundamental for the old continent’s transformers. At any rate, apart from the price swings, there have been no procurement issues, national aluminium institutions and associations greatly helped in overcoming the bureaucratic difficulties generated by the effect of the sanctions. The problem of tariffs on the importation of raw metal is still being discussed in Europe, it is absurd that a tariff should be maintained on such a raw material as primary aluminium which EU companies absolutely need because not enough of it is produced within the Union and which is artificially priced at higher levels with respect to other areas in the world, that is, with respect to our competitors. Therefore, having established that it is impossible to act on tariffs on the import of semis, we are in such a position as to have to watch helplessly the invasion of profiles from China, Russia, Turkey, unfortunately while being aware of the fact that the tariff on the primary metal does not protect European smelters from shutdowns at all: recent news as to the discontinuing of primary production plants in Spain confirm this fact. Based on many rumours head here in Brussels, the European Aluminium Association seems to be receiving from many associated operators in the downstream sector the input that the elimination of tariffs on the raw metal should no longer be hindered: we should hope that finally common sense will prevail and lead to considering even the interest of downstream operators and not just the producers of raw metal.